Blog

A collection of insightful and informative articles from Myerson Wealth's “Recipes for Success” newsletter

A collection of insightful and informative articles from Myerson Wealth's “Recipes for Success” newsletter

Without possessing a crystal ball to help us gaze into the future, we’ll never know when a down market may hit our investment portfolio. Let me tell you about John, who sure wishes he had said crystal ball. A week after retiring from a 40-year career, John started planning his dream vacation to kick-start his retirement. Unfortunately, that same morning marked one of the worst days in market history: John’s retirement portfolio dropped 15% by market’s close. Instead of looking forward to his vacation, he faced the grim reality that his retirement funds may not sufficiently sustain him in the years to come.

John, like many others, planned his retirement around a certain age, hoping to secure enough money to live a very comfortable lifestyle. Prior to the market crash, when reviewing his retirement portfolio, he assumed a constant rate of growth that allowed his funds to last his lifetime. The rate he used was an average return based on market performance over time, but John had forgotten lessons learned from previous market corrections: The market does not act in a consistent manner.

A sequence of returns—market gains and losses—makes up the average rate that is used to illustrate a portfolio’s ability to deliver planned retirement distributions. Without knowing when a drastic drop may come, a negative market-return during retirement can severely impact your portfolio’s ability to recover. This is particularly true if distributions are needed to maintain one’s lifestyle at the time the portfolio is depressed, as those withdrawals will never have the opportunity to recover. Now, John is concerned that his retirement fund will not provide him with sufficient living expenses as he had planned.

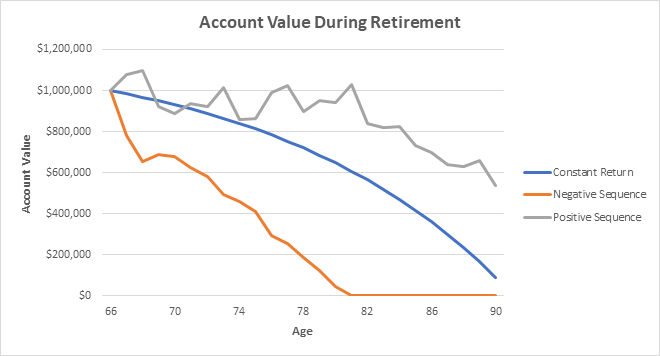

The graph below shows an example of how sequence of returns works.

|

This graph shows how a sequence of returns may affect a retirement account. All assume a starting balance of $1 million and taking out $80,000 per year. The blue line assumes a constant annual 7% return. The orange and gray line both assume a 7% average return through age 90 but are made up by a random sequence with positive and negative years. The orange assumes the same sequence as the gray line but reverse starting order, beginning with negative years. This graph is strictly for presentation purposes and not based on actual market performance. |

Lisa retired around the same time as her co-worker John, but she woke up that morning feeling relieved. She wisely diversified a portion of her money into a product that mitigated downside market risk: Indexed Universal Life (IUL). An IUL policy gives clients market growth exposure while eliminating downside risk. But how? Indexed Universal Life comes with various account options (usually tied to the S&P 500 Index) that offer, at worst, a 0% floor in years the market loses value, but provide market upside in years the index is positive. Safety from downside risk isn’t “free,” however. An IUL policy gives clients that 0% guaranteed floor but in return either places a cap on or provides a participation rate for a percentage of the gains. Given the market’s history, while we can never predict when the significant swings will occur, we know that there will be many more years of positive returns than there will be negative. And with a zero floor in years that the market does correct, long-term upside can be significant (and all tax-deferred, but that’s for a separate article).

Diversification between Lisa’s investment portfolio and an IUL gave her multiple income streams to choose from during retirement. Instead of accessing money from her portfolio that had just taken a market hit, Lisa accessed the funds from her IUL policy that didn’t suffer a negative impact. Now, she can allow the money inside her investment portfolio to recover without depleting it even further.

Contact Myerson Wealth today to see how an IUL policy can help diversify your retirement portfolio.